Echoing our opening salutations from last year’s 1Q report - We hosted our Annual Investor conference just prior to pressing “send” on this report and we thank you for your attendance. We are grateful for your continued commitment to Griffin Partners.

In this report we will touch upon a few of our industrial markets that continue to see positive demand fundamentals. An update on the debt market and overall CRE transaction volumes occurring this past year is also included. A pivot in the capital markets is appearing as we endure a new normal with “higher for longer” interest rates. The CRE sector is resilient, and the market has begun to adapt. In turn we will see more trades (transactions & Griffin opportunities) in 2024 relative to the dearth of CRE transactions in 2023. Lastly, we will provide a few takeaways and internal statistics on transaction volume for office assets and remind our readers about the “haves” and “have nots” defining office assets across our target markets.

The Table of Contents below can assist with navigating to a preferred section or getting a quick general take.

- Fund Updates: High level news on Fund activity.

- Real Estate Market Conditions: In this section, we will review:

- Industrial Spotlight – Houston, Dallas, Nashville and Raleigh

- Lender Capitulation – So you're saying there's a chance?

- Office Trades – Unpacked

- Macro Economic Conditions:

- Stagflation, is it here or on the way?

Fund Updates

Fund III:

We are continuing negotiations with two banks regarding four existing loans with either near term maturities or technical defaults resulting from higher interest rates. The negotiations have been difficult but constructive; however, the final terms will require additional capital in some cases which will be dilutive to existing owners. It is too early to know the exact terms, although we will continue to be transparent with the outcome and will provide more details as allowed per our pre-negotiation and confidentiality agreements in place with each lender.

Please refer to the Manager’s Letter later in this report for additional specifics on the assets in Fund III.

Fund IV:

Airport 6, Charlotte, NC: As mentioned last quarter, one of the six assets in this portfolio, Twin Oaks, was formally under contract to sell. Unfortunately, the Buyer did not perform. Irrespective of buyer non-performance, we’ve continued to focus on stabilizing the rent roll and we are very optimistic that in our next report we will be able to provide positive leasing news that will allow us to revisit a potential sale to continue to harvest gains and reduce our debt exposure for this portfolio of assets.

Saturn Crossing, Nashville, TN: We are happy to report this past quarter we executed our first lease at this Project. The new tenant, Gravity Media, is a global media production and broadcasting company based in the United Kingdon. The company has leased 34,560 square feet (17% of the Project) for a sixty-three (63) month term. This lease commenced upon execution, prior to the build-out and occupancy; and the tenant will begin paying rent on August 1, 2024, the end of the free rent period. Bravo to the TEAM on executing this new lease. Lastly, we are encouraged by our leasing momentum, and we anticipate providing more good news to share in our next quarterly report.

Please refer to the Manager’s Letter later in this report for additional specifics on the assets in Fund IV.

Real Estate Market Conditions

The following Griffin Partners Take-Aways are our latest observations on current commercial real estate (“CRE”) market conditions. It’s my pleasure to mention that David Hotze on our TEAM contributed significantly to the Real Estate Market section of this quarterly report:

Industrial Spotlight – Houston, Dallas, Nashville and Raleigh:

- Each of the markets in the headline above continues to see positive industrial CRE fundamentals as demand persists in outperforming some more cautious assessments. For example, in a recent report delivered by Prologis, the world’s largest owner and operator of industrial real estate, noted in its quarterly earnings call that Texas was a highlight of their portfolio due to the “unique demand drivers.” The following are a few “snip-it’s” from research reports we review to help develop our opinions and thoughts on supply and demand characteristics for each of the markets mentioned:

- Houston: We are continuing to see positive signs in the leasing market with new leases being executed on a weekly basis and at rates which continue to support our latest speculative industrial development in Houston. Per the latest GreenStreet 1Q-2024 report “….Houston container volumes at the Port of Houston have grown substantially since 2019 as companies have looked to diversify their supply chains. Once predominantly export-driven due to the city’s energy sector, the market has seen a ~65% increase in import volume compared to FY 2019.” As of 1Q-2024, per GreenStreet’s latest data, “….demand remains robust with over four million square feet of net absorption recorded in the quarter. Houston’s industrial occupancy rate is ~95%, and vacancy appears to be nearing a peak. The active under construction pipeline has dropped below 10 million square feet (~1.7% of total market inventory) for the first time since the pandemic following multiple years of high supply growth.” These CRE points are all positive signs for a tightening market with limited new supply through 2025.-Dallas (DFW): Per GreenStreet 1Q-2024 “….Demand remains positive with DFW absorbing over two million square feet in 1Q24, though elevated supply growth has lifted vacancy rates from ~4% to ~6% over the past two years. Supply growth is concentrated in South Dallas, North Fort Worth, and DFW Airport…. and these submarkets comprise most of the larger bulk warehouses. Despite a higher concentration of near-term supply growth, DFW Airport is still expected to outperform over the long run. Other submarkets that are land-constrained and are key distribution hubs (with high transit connectivity) such as Central / East and Great Southwest / Arlington, should also see comparatively strong rent growth in the coming years. Overall, elevated supply growth with vacant deliveries will keep a lid on rent growth, but the MSA is less likely to see material reductions relative to the national average due to demand strength.” As GreenStreet accurately characterized, the South Dallas submarket has seen an abundance of new supply of “larger bulk warehouses”, buildings generally greater than 500,000 square feet. We continue to have conviction that our Port 45 asset (delivered earlier this year) will be leased in the very near future with the current leasing and potential user pipeline continuing to produce requests for proposals (RFP) to lease or user sales. Further, overall rental rates in South Dallas have outperformed our expectations with starting rental rates +/-20% above our underwriting.

- Raleigh: Per CoStar 1Q2024 Report: “…Raleigh is the fourth-fastest growing major market in the country, and population growth will continue to drive additional demand from e-commerce tenants and third-party logistics companies. Rent growth in Raleigh has decelerated over the past year, but the market's annual rent growth of 6.3% is still slightly above the market's 10-year annual average of 6.0%. The market has 3.1 million SF of space under construction, which represents a 3.0% expansion of the market's total inventory. While that is a relatively high level of construction, the market's pipeline is down significantly from a peak of 6.1 million SF in the middle of last year. Much of the rise in vacancies has occurred in larger industrial buildings. Meanwhile, industrial buildings under 100,000 SF have vacancies of below 5%...” The tightening of supply in the shallow bay industrial buildings continues to drive Griffin Partners’ strategy to develop new assets in close proximity to city centers within 20-30 minute drive times of the city center. Our most recent search for land for new development continues to be along major trade routes such as Interstate 40 just west of the Raliegh-Durham market.

- Nashville: Per JLL 1Q-2024 Report: “…The Nashville industrial market recorded 3.7 million SF [of absorption] for Q1 2024. The Southeast industrial submarket accounted for 37% of all trailing four quarters leasing activity, ahead of the East at 32% by only a few percentage points. There are 4.0 million SF of tenant requirements currently in the market which will lead to continued strong leasing activity. Another 4.5 million SF of spec deliveries are expected in 2024 and early 2025, and with a shrinking pipeline, vacancy is expected to drop, and landlords will continue to push asking rates higher…the current construction pipeline is at a four-year low as groundbreakings have fallen three years in a row…”. This bodes well for Griffin Partners’ latest project, Earhart Logistics, in the East submarket. We are happy to report the first building totaling +/-860,000 square feet is under construction with the slab being poured as we deliver this report. The second and larger building will start construction just a few weeks after slab completion of the first building as contractor sequencing is paramount in maintaining our fast-paced timeline due to the sheer size of the project (+/-2,100,000 SF). We anticipate delivery in the first and second quarters of 2025 and as mentioned new supply is at a 4-year low (competition) and deliveries at this time in the submarket will be almost nonexistent.

Construction Financing – “so you’re saying there’s a chance?”

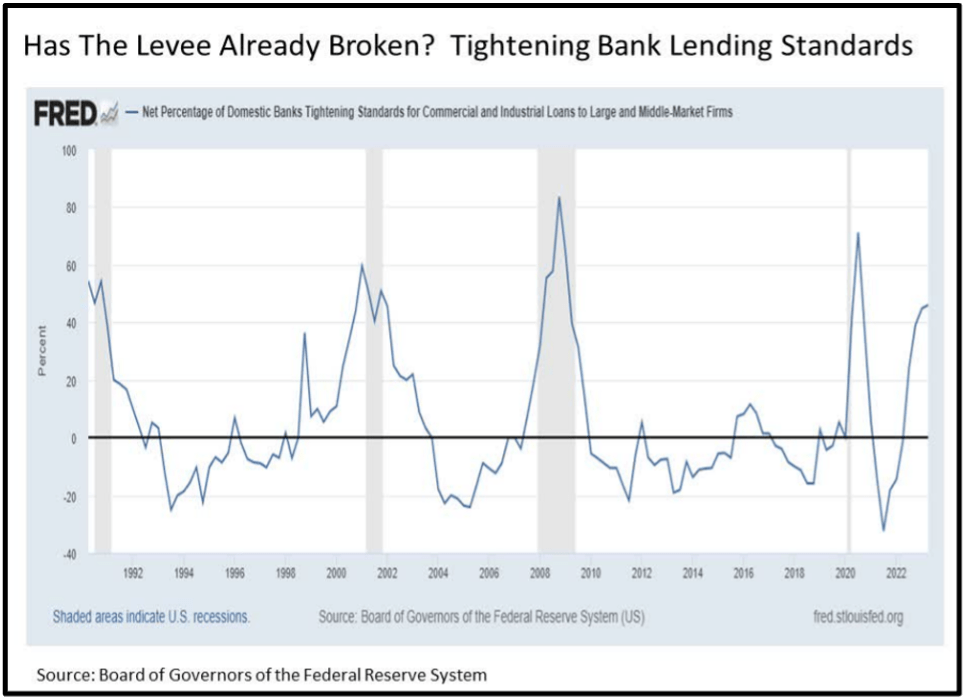

- In prior quarters we shared that the debt markets have slowed, and in our 1Q-2023 report we presented the following chart below “Tightening Bank Lending Standards”, a Fed Reserve Board Senior Loan Officer Opinion Survey (SLOOS).

In our 1Q-2023 report we summarized this “…. chart measures the willingness (falling line) or unwillingness (rising line) of financial institutions to make commercial loans. This rising line on the far right of the chart doesn’t paint a very good picture for the rest of 2023 lending environment…” As suspected, most of 2023 lending standards remained rigid and overall debt issuance stalled severely compared to the previous 24 months on new loans for both existing assets and new construction. Further, in addition to the “cost” or “standards” required for new construction loans, these elevated lending standards tipped the scales higher for yield on cost metrics; in turn forcing developers to drop land sites under contract and effectively go “pencils down” for most of 2023.

Click here to request the full Q1 2024 Report.

Fast forward 1-year to 1Q-2024, as you will see in the chart nearby, debt tightening standards for CRE Loans have thawed. As of YE 2023, real estate values and interest rates have shown signs of stabilizing showing a “light at the end of the tunnel” approach for a healthier debt market in 2024. Since 4Q-2023, real estate lenders are in the early innings of loosening standards across all sectors (falling line), also including construction lending. As an example from recent experience, we are pursuing a speculative industrial development west of Raleigh and we’ve recently executed, just prior to this publication, a construction loan term sheet at 60% LTC, non-recourse, with tighter spreads than late 2022 and all of 2023. While capital costs remain elevated, limiting potential new development, all signs point to the beginning of a recovery in the debt markets and overall transaction volume.

Click here to request the full Q1 2024 Report.

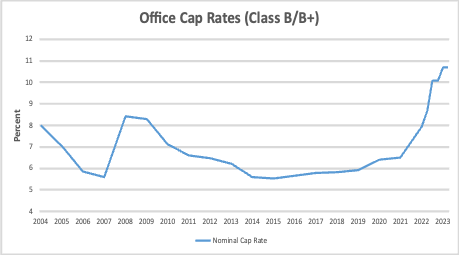

- In previous reports, we have extensively covered the bifurcation that is occurring in the office sector (re: the haves vs. the have nots) and the fact that older vintage (1980-1990 era or older), more commodity product is bearing a significant portion of the total vacancy in the office market (per CBRE total year-end 2023 vacancy was 18%). These “have nots”, when they do trade, continue to trade at significant discounts compared to newer, higher quality office properties located in suburban/urban areas with strong in-fill locations. As the chart nearby shows, since mid-2021, average nominal cap rates for Class B/B+ office product in the U.S. have expanded from a 6.5% cap rate to a 10.75% cap rate today (wow!).

Unlike the cap-rate expansion in 2007-2008, office obsolescence, tightening debt standards, and post-COVID work from home fundamentals have impacted primarily institutional investor interest, and “higher for longer” interest rates are also impacting these assets in an outsized manner. The following are a few anecdotes from the market for these older vintage “have nots”:

- Lender interest and debt availability is extremely scarce. Our team continues to track the market closely, including the commodity product being listed for sale. Many of these assets, especially those with lower occupancy, were being marketed with the knowledge that financing a purchase would be nearly impossible and therefore transactions are mostly “all-cash” purchases, driving down values equating to double digit yield on costs and high unlevered returns.

- A good portion of this type of product (Class B) may never reach their historical occupancy levels again or are destined for other uses (conversions or covered land plays). Throughout 2023, our team tracked more than 130 investments fitting these criteria in our target markets and only 35 of these office assets traded (~25%). While some of these owners were no doubt able to restructure their debt, or extend loans, the lack of liquidity and trades suggest that structural vacancy for the office sector will continue to remain for the foreseeable future. Without sufficient capital to “amenitize” and lease these buildings, along with competition from newer vintage assets, a good portion of these assets will be or have already been rendered obsolete leading to higher structural office vacancy for years to come.

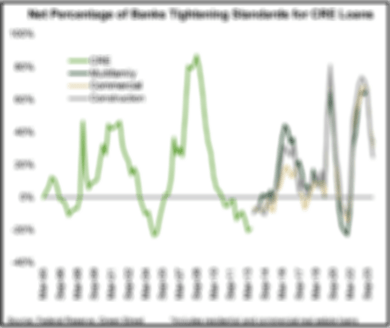

- In contrast, newer vintage, functional office buildings with strong historical fundamentals and good locations continue to garner outsize leasing demand as compared to Class B, commodity product (see chart nearby).

As we have mentioned in the past, any potential office investment we make, if any, in Fund IV will have to fit an extremely narrow box. This box includes newer vintage (>2000), above average historical occupancy, strong in-fill location attributes within a mixed-use environment, and very high walkability to name a few. The following are a few anecdotes from the market for these newer vintage assets, or the “haves” in the marketplace today:

- Debt for the best-in-class office product can be made available, but it is expensive and difficult to source. Nearly all our regional banking relationships have turned off the spigot for new office loans and refuse to entertain new office loans. A buyer must look toward Debt funds, CMBS or Insurance companies for financing. Even then, given the lack of lender confidence in office today, some form of recourse will be required.

- As the CRE market continues to reset and office owners now have more realistic expectations on value, the “bid-ask” spread is beginning to narrow as capitulation has begun. A smattering of trades is beginning to occur for the best, high-quality product. The Griffin TEAM looked at over 300 office offerings in 2023 and bid on only three that fit our stringent criteria. A couple of examples below:

- Our TEAM will continue to review (and possibly bid on) what we believe are compelling discounted opportunities for new, best-in-class office assets within suburban areas that are poised to continue to outperform for the foreseeable future. Higher quality, newer office assets in the right locations should continue to achieve higher leasing demand and are at a lower risk of future obsolescence.

Griffin bid on a 2009 vintage, 175,000 SF mixed-use office building in Cool Springs, TN, just outside of Nashville. The building was 95% leased, surrounded by a multitude of walkable amenities, and located within a high-end affluent pocket. This building sold in Q3-2023 at a +/-9% cap rate (more than a 200-basis points inside commodity B/B+ office product).

Griffin bid on 2000 vintage, ~50% leased, 140,000 SF office building in The Woodlands, TX. Similar to the building in Nashville, the building was high-quality and located in an affluent area near walkable amenities and was in a submarket with no planned supply and the second lowest vacancy rate in the Houston MSA. The building was awarded to all cash buyer and is expected to trade at an +/-8% cap rate with approximately an 11% yield on cost at a fraction of replacement cost.

Macro-Economic Conditions

Are we at risk of “stagflation?” There seems to be an elevated level of discussion in the financial and economic press about the possibility of stagflation in the U.S. What is stagflation? Generally, it can be understood as high inflation at the same time as low output (GDP). The economists at Wells Fargo recently wrote a piece indicating that the U.S. may be at risk of a period of stagflation now, at least as they define it. Their definition for low output is two or more consecutive quarters of GDP growth below the average GDP growth for the prior economic cycle. Their definition of high inflation is a bit more dynamic, but suffice it to say, recent levels of inflation qualify.

Using this definition, the Wells Fargo piece identifies 13 instances of stagflation in the U.S. since 1950 and highlights the unique challenges each instance posed to monetary policymakers. It notes that six episodes occurred in the 1970s due to oil price shocks, imbalanced fiscal and monetary policies, and rising labor costs, which led to high inflation and low output growth. Notably, we have imbalanced fiscal (highly expansionary) and monetary (restrictive) policies now. We also have treasury (Yellen) running a shadow monetary policy by flooding the market with short-term bills instead of longer-term bonds.

Historically, stagflation has been met with accommodative monetary policy to support employment, despite high inflation. The effectiveness of this approach varied depending on the underlying causes of inflation and the economic structure at the time.

The team at Wells Fargo then questions whether the current low unemployment rate and swelling fiscal deficit could lead to stagflation in the near term, drawing parallels with past severe episodes influenced by external factors like oil price shocks and expansionary fiscal policy. It mentions significant inflation momentum since 2021, with CPI reaching "severe" territory in Q4-2022, and a slowdown in real GDP growth in the first half of 2023 and again in Q1-2024. The report forecasts a potential end to the current stagflation by Q4 of this year but warns that the risk remains elevated if the labor market doesn't loosen as expected. One risk is that the path of inflation is uncertain due to geopolitical risks and other structural inflation pressures.

Wells Fargo: “We suspect government purchases will moderate in coming quarters, which will dampen its contribution to real GDP growth. Though the unemployment rate is at a decades' low today, we expect the labor market to gradually loosen as restrictive monetary policy continues to filter through. Less marked job growth will weigh on real disposable income, further dampening real GDP growth and inflation by pressuring consumer spending.”

Continuing: “Should our forecast come to fruition, our framework says the current bout of stagflation will end in the fourth quarter of this year. What was once a severe episode of stagflation in 2022 has downgraded to a mild case in the opening innings of 2024, but the path of inflation remains uncertain. We suspect the risk of stagflation remains elevated in coming years, especially if the labor market does not loosen as presently anticipated.”

Last quarter we continued our commentary on the mixed signals coming from the labor market, in particular the divergence between the establishment and household surveys in depicting U.S. employment trends, with the former showing robust growth and the latter nearly stalling.

The just released May jobs data shows an even greater divergence with the gap between the number of total jobs in the two surveys hitting a record 9 million. See nearby chart. As a reminder, the widely watched establishment survey is sampling and estimating the number of people on company payrolls, and the household survey is using a smaller sample of contacted households to estimate the number of people who have jobs. The household survey is demographic, including agriculture and self-employed workers, while the establishment survey focuses on industry employment, excluding these groups. Reasons for the discrepancy include the business birth-death algorithm (new businesses and closed businesses) in the establishment survey, inaccuracies in population estimates, the smaller sample size of the household survey, and importantly the relative gain of part time jobs versus full time jobs. In fact, full-time jobs have declined over the past year, and all the job growth has come from part-time jobs. A large amount of the discrepancy comes from the jobs assumed to be created by the establishment survey’s birth/death model. The Bureau of Labor Statistics (BLS) does not attempt to reconcile the output from its birth/death model until the following year. We remain a bit skeptical that the labor market is as healthy as headlines indicate.

Both the headline and core PCE inflation rates are at 3.0% on a smoothed six-month annualized basis. This core inflation rate is above the 2% Federal Reserve target. The Cyclical Component of GDP, which includes residential investment, business equipment investment, and durable goods consumption, declined over the last three quarters from 3.1% to 1.8% to 0.6%. Real personal income excluding government transfer payments was revised lower by $92 billion, indicating a significant decrease

The Aggregate Coincident Index of real growth was revised lower in April to a growth rate of 1.1%, suggesting a clear and undeniable step lower in Q1 in terms of real growth. The nominal growth level imputes a growth rate of 4.8%, which is below the overnight Fed Funds rate for the 11th consecutive month. See nearby chart. This suggests the shift from other deposits in the banking system to money market funds and CDs is continuing, and there is a lack of new real credit being extended to consumers and small businesses by commercial banks. With the overnight Fed policy rate above the trend-line level of nominal growth, there will very likely continue to be a shift from other deposits (ODL) in the banking system, to money market funds and CDs. Real ODL, real bank credit and real bank loans all remain negative on a year over year basis, rendering the commercial banks “out of the game” in terms of extending new real credit to consumers and small businesses. A chart of loan growth at the major banks nearby illustrates this condition, and it does not bode well for economic growth.

There are a couple of elements of good news, although they may offset each other somewhat. Core CPI is likely to rise by 0.3% in May according to Wells Fargo Economics, similar to April's increase, which would bring the year-over-year rate to a three-year low of 3.5%.

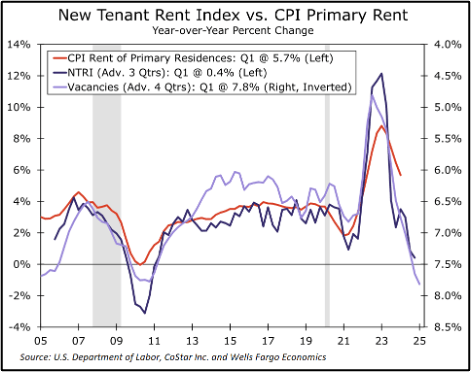

Despite some opinions to the contrary, there is evidence that the first quarter's inflation spike has subsided, with expectations for monthly readings to gradually trend lower. As we highlighted two quarters ago, many economists are now focused on expectations for shelter inflation to slow down and contribute to the overall reduction in core CPI over the next year. Private-sector measures of apartment rents are running below pre-pandemic rates, and the apartment vacancy rate, which has historically led CPI rent of primary residence by approximately 3-4 quarters, has yet to peak this cycle. The Bureau of Labor Statistics' New Tennant Rent Index (NTRI) indicates rent growth for newly signed leases of primary residences is slowing to under 3% over the next year. It may take longer for Owners' Equivalent Rent (OER) to cool because of high interest rates and a shortage of single-family housing. The nearby chart illustrates the accelerating vacancies and declining NTRI.

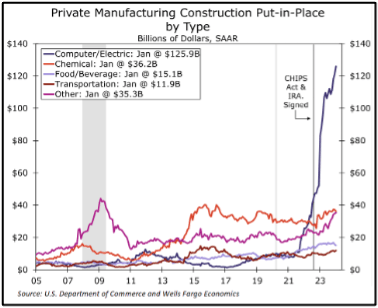

The other bit of good news may be contributing to higher inflation. The U.S. is experiencing a significant increase in high-tech manufacturing construction, call it a boom because it is. This boom is reshaping the economy and shortening global supply chains. The boom is not expected to lead to massive job growth in manufacturing but will enhance technical capabilities and potentially increase productivity. A substantial portion of the construction spending is in the computer, electronic, and electrical manufacturing sectors, partly driven by the CHIPS Act to boost domestic semiconductor production. The nearby chart shows the outsized gains in computer and electronic manufacturing facilities. While the CHIPS Act will taper off in a few years, this burst in investment could prove to be one of the more productive government expenditure programs, although it is way too early to tell, and the U.S. government does not have an unblemished record in picking winners.